“Overnight a family could have to pay a further £563,600 in IHT” - Seán’s Times Interview

The government took £8.2 billion in inheritance tax last year. Next year this will be higher and 38,500 people are projected to pay more IHT when pensions fall into the estate in April 2027.

Many people are totally unprepared and have no idea.

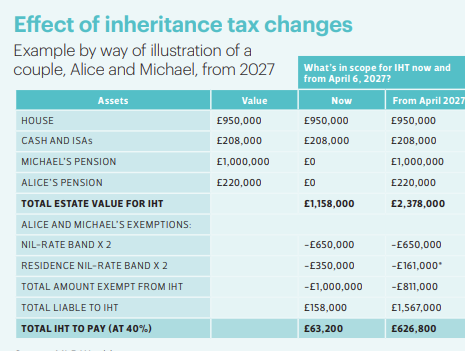

In the Times article, Seán explains how overnight a family could have to pay a further £563,600 in IHT. Jumping from £63,200 to £626,800!

Find out how in the full article below.

Next year pensions will undergo a major change, and advisers are preparing their clients early to avoid a substantial tax hit.

Until now, pensions were often used in legacy planning as a way for families to pass on savings tax-free to their beneficiaries, but this avenue is closing. From April 2027, most unused pension funds will form part of an individual’s estate for inheritance tax (IHT) purposes, meaning a potential 40% charge.

Financial advisers such as Seán Standerwick of MLP Wealth in Banstead, Surrey, are making sure their clients are prepared for this shift. He says: “I’m discussing this with a lot of my clients as it can have a massive impact.” But with some careful planning, Standerwick says he is able to help clients make use of other reliefs so they can still pass on as much of their wealth as possible to their loved ones rather than the taxman.

Pension tax rules are complex and it can be difficult to understand whether or not you are affected by the reforms. Those with final salary or defined benefit pensions, which pay out a set amount per year over the course of retirement, are not impacted by the rule change because they would not usually be able to pass on their pension at death, although a spouse or dependent child might continue to receive a proportion of their income. The same applies to any pension that has been converted into an annuity to provide an income for life. However, any pension pot left over after buying an annuity will be in scope for death duties from next April.

Most families will not be liable for IHT even after the changes, but the government’s forecasts suggest that, in the first year following the reforms, 38,500 estates will pay more than they would have done under previous rules. It says the average IHT liability is expected to increase by around £34,000 when pension assets are included.

However, the cost of doing nothing could run to hundreds of thousands of pounds in the worst examples, warns Standerwick. A couple with a combined pension pot of £1.2 million, a house worth £950,000 and ISA investments worth £208,000, would see their IHT bill jump by £563,600 overnight, from £63,200 to £626,800.

Standerwick is using a variety of planning tools to help his clients safeguard their savings for their children and grandchildren. One such strategy takes advantage of business relief, which allows up to 100 per cent of a company’s assets to be passed on to successors without paying IHT. It is designed to help businesses continue trading after the death of one of the owners. Standerwick has helped several clients find appropriate investments, so they can use this relief as part of their inheritance planning.

He says: “In cases like these, we can show that by putting in place the right structure for their investments at the outset, we can save clients thousands of pounds in taxes further down the line.”