Trying to time the market could have cost you nearly £100,000 – here’s what to do instead

“Is now a good time to invest?” is one of the most common questions we get asked by clients.

While it’s something we are used to hearing at all times, it’s a particular concern when markets feel uncertain, headlines are alarming, and everyone on social media seems to know exactly what’s coming next.

However, the honest answer is: “We don’t know.”

That’s not because we’re not as knowledgeable or experienced as other advisers, but because nobody knows what markets will do in the short term.

While that may feel like an unsatisfying response, it’s also one of the most important truths in investing. Over the short term, markets are wildly unpredictable, while over the long term, historical trends are easier to discern, and they point in one direction: towards growth.

The problem is that our brains are not wired for long-term investing. They’re wired for survival. So, when markets fall, we feel danger. When headlines are persistently negative, our instinct is to act. But successful investing is often about doing the opposite of what emotion tells us to do.

Read on to find out how costly attempting to time the market can be and what you should do instead.

Attempting to “time the market” can lead to significant losses

“Timing the market” is when an investor tries to either enter or exit the market at just the right moment to capitalise on an impending rise or fall. The aim is either to buy low just as a stock is set to soar or sell high as it is about to dip.

In theory, perfectly timing the market can lead to considerable returns, but in practice, you’re far more likely to misjudge your attempt and lose out, which can cost you in the long term. Indeed, even missing just a few days by exiting at the wrong moment can be costly.

Let’s look at a simple example.

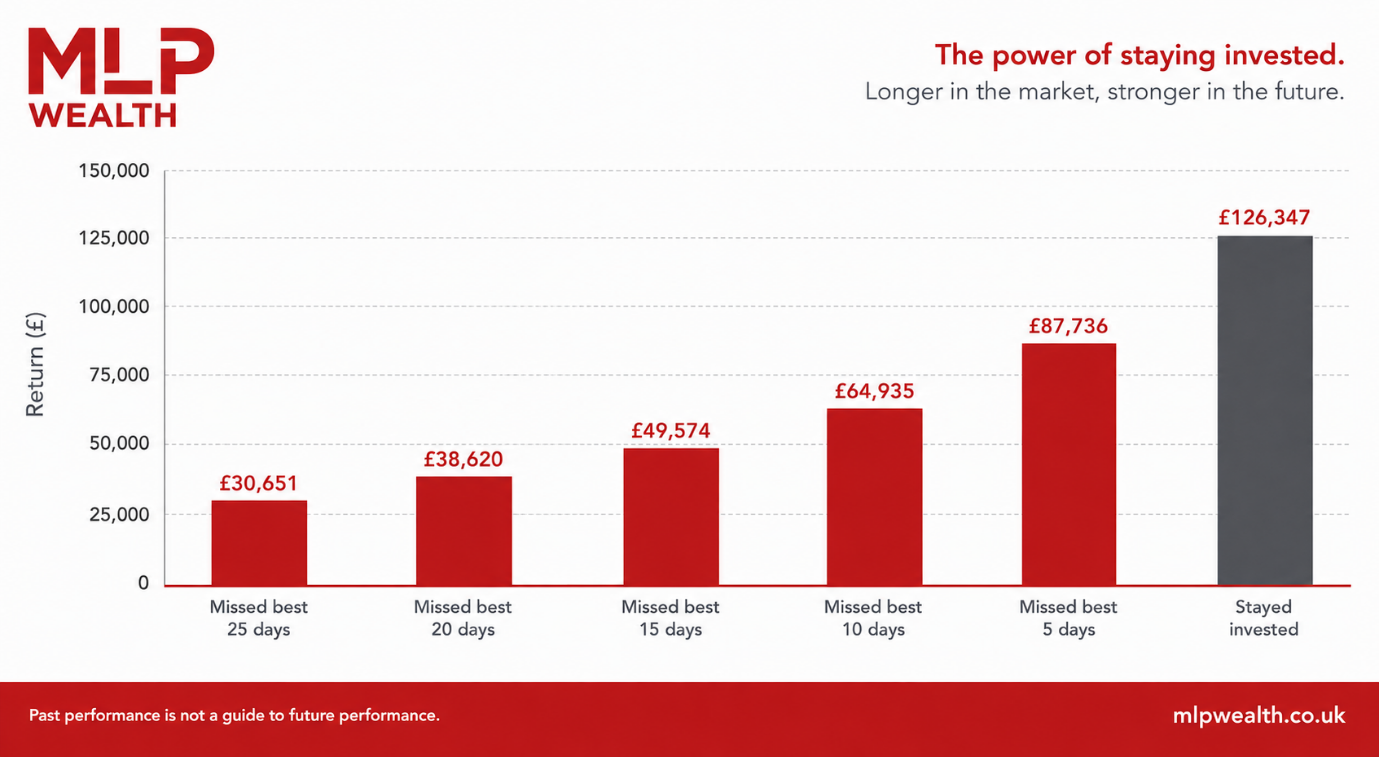

If you had invested £10,000 in global equities through the MSCI World Index and left it invested for 30 years between 1 January 1996 and 31 December 2025, your investment would have grown to £126,347.

However, if you had attempted to time the market over that period, and in doing so, you missed out on some of the index’s best days by exiting, the same investment would have yielded:

£87,736 if you missed the 5 best days

£64,935 if you missed the 10 best days

£49,574 if you missed the 15 best days

£38,620 if you missed the 20 best days

£30,651 if you missed the 25 best days.

So, the difference between staying invested and missing just the best 25 days was £95,696. Missing less than a month of investment days over two decades would have reduced your wealth by nearly £100,000. Even missing five days would have seen you almost £40,000 worse off.

And crucially, the best days in the market often happen very close to the worst days, as the returning confidence after a dip often leads to a surge. This means that investors who panic and move to cash after a fall frequently miss the rebound that follows.

The graph below shows the results of the study into missing just a few of the best market days.

Source: Quilters

History shows that exiting during dips and chasing high performers rarely leads to successful outcomes

Attempting to time the market is typically done in order to cut losses or chase the latest trend. However, history shows that this rarely leads to success.

When it comes to cutting losses, markets have faced wars, recessions, inflation spikes, political crises, pandemics, and banking collapses. Yet over long periods, they have historically rewarded disciplined and patient investors who chose to ride out downturns rather than exit for cash.

Research by Schroders found that investors who moved to cash in 1929 after the first 25% drop during the Great Depression wouldn’t have broken even until 1963. Meanwhile, those who stayed invested would have recovered by early 1945.

Similarly, investors who switched to cash after the initial 25% fall in 2008 would still not have recovered their losses at the time of the study in 2024, while those who stayed invested would have recovered by around 2013.

Furthermore, investors who attempted to jump on a bandwagon and pursue the latest high-performing stocks have also been historically unlikely to find success.

Another study by Schroders found that in 12 of the 18 years between 2005 and 2022, not a single US stock that was a top 10 performer in one year also made the top 10 in the next. In five of the other six years, only one managed to make it again, and in the other year, three did.

So, rather than attempting to cut your losses or catch a quick gain, maintaining patience and discipline has historically proven to be a more successful approach to investing over the long term.

Certain investing strategies can improve your chances of long-term success

Rather than trying to time the market, there are several evidence-based investing strategies that can improve your chances of long-term success. These include:

Adjusting your investment risk based on your time horizons. Longer-term goals have more time to ride out fluctuations and can be more suitable for higher-risk investments, while medium- and short-term goals are typically better suited to lower-risk alternatives.

Diversifying your portfolio. By spreading your investments across different asset classes, regions, and sectors, you can offset losses in one area with gains in another, providing a more stable path to long-term growth.

Clearly defining your long-term goals and planning how to achieve them, so you know why you’re investing and the time horizon involved.

Focusing on your long-term plan, rather than reacting to short-term market movements.

Ensuring you have cash or liquid assets to cover your short-term needs, so you don’t need to draw on your investments at challenging times.

The biggest threat to long-term investment success is often not the market, but investor behaviour and emotional decision-making.

We can help you build a financial plan that enables you to benefit from the market’s best days while also ensuring you remain on track when markets become more challenging.

To speak to a financial planner, get in touch.

Email info@mlpwealth.co.uk or call us on 020 8296 1799.

Please note

This article is for general information only and does not constitute advice. The information is aimed at individuals only.

All information is correct at the time of writing and is subject to change in the future.

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.